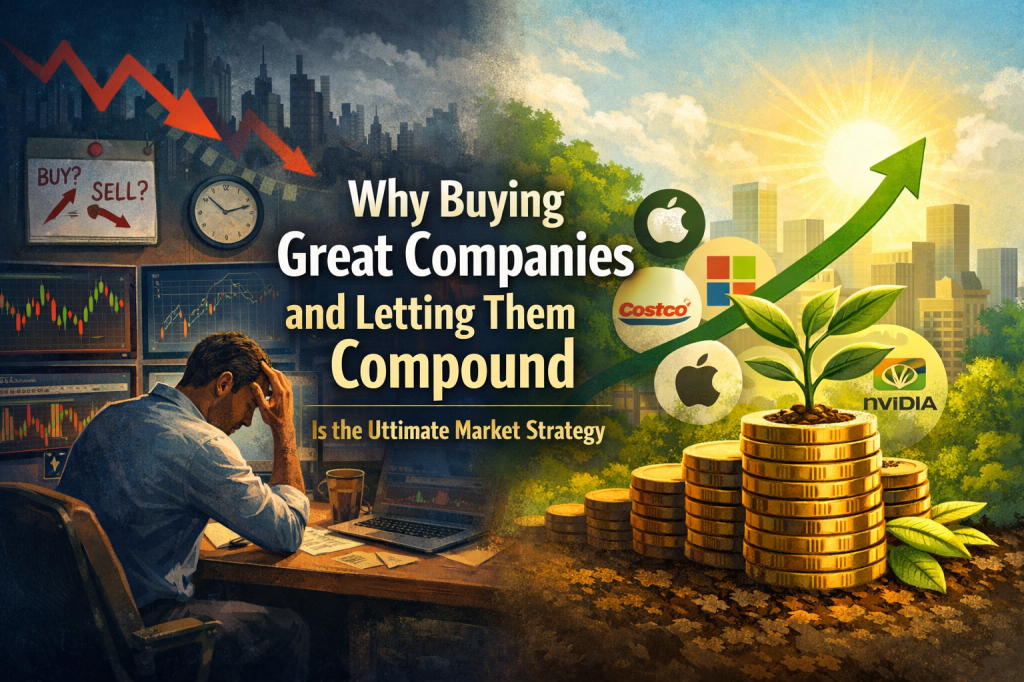

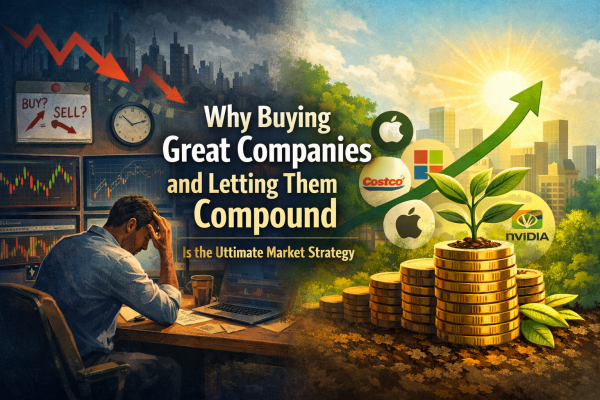

Every investor eventually reaches a crossroads. One path is crowded, loud, and filled with flashing indicators, prediction models, and people convinced they’ve cracked the code to timing the market. The other path is almost boring in comparison: buy excellent companies and let compounding do what human intuition rarely can. And although the louder path feels more exciting, it’s the quieter one that consistently builds real wealth.

Let’s walk through a story that shows exactly why.

Back in 2010, two analysts—David and Elena—started investing at the same time. They had similar financial backgrounds, similar salaries, and similar ambitions. But their philosophies couldn’t have been more different.

David was determined to forecast the market. He believed that with enough study—RSI thresholds, MACD crossovers, sentiment cycles, volatility squeezes—he could “catch the uptrends and avoid the downtrends.” He watched the news like it was oxygen. A hint of geo-political tension? He reduced exposure. A hawkish Federal Reserve headline? He sold risk assets. A rally that seemed too good to be true? He trimmed profits before the “inevitable” pullback.

In theory, it made sense. In practice, timing the market demands a perfection very few humans can sustain.

In 2011, a brief correction scared him out of the market. He stayed in cash for nearly a year waiting for a “safe re-entry” that never appeared. In 2013, he bought back in late—and got hit with volatility almost immediately. By 2015, interest-rate noise pushed him to unload positions right before a strong multi-month run. Then came 2020, the year that humbled even seasoned traders. The moment the market cracked, he went all to cash for “just a few weeks.” The fastest recovery in modern history launched without him.

By missing only a handful of the best market days, David cut his decade-long returns down dramatically. Most investors underestimate how powerful those handful of days are. Historically, missing just the ten best days in a decade can slash your total return by more than half. Those days don’t announce themselves; they show up suddenly, usually when sentiment is darkest. And like clockwork, David was always waiting for clarity during the exact moments that required courage.

Elena, meanwhile, played a different game.

She ignored the daily noise and focused on what never goes out of style: great businesses. Instead of trying to predict economic weather, she studied fundamentals—cash flow strength, competitive moats, leadership quality, long-term demand drivers, and the ability to innovate. She wasn’t buying charts; she was buying engines.

She picked Apple not because of a breakout pattern, but because of customer loyalty and relentless product evolution. She bought Microsoft because cloud computing was clearly the backbone of the next decade. She added Costco because disciplined companies with strong membership models outperform in both recessions and booms. And she held Nvidia because she understood early on that data, automation, and AI needed infrastructure—and Nvidia built it better than anyone else.

She didn’t trade often. She didn’t panic during corrections. As long as the business continued executing, she stayed put.

Her strategy required patience, not perfection.

Instead of trying to be right every week, she only needed to be right once: in her decision to own great companies for the long haul. And compounding handled the heavy lifting from there.

By 2020, the contrast was stark. David’s active timing produced about $17,000 from his original $10,000. Elena’s patient compounding built roughly $44,000 from the same starting point. And the longer the timeline stretched, the wider the gap became—because compounding accelerates, multiplying discipline into exponential results.

This is the real lesson: timing requires you to be right twice—when to get out, and when to get back in. Compounding requires you to be consistent once—own great companies and let them grow.

Buying excellent businesses is one of the few strategies that neutralizes emotion, bypasses the need for perfect foresight, and aligns naturally with expansion periods you can’t predict but will always benefit from if you stay invested.

Great companies innovate. They reinvest. They scale. They survive downturns and thrive in recoveries. They compound, quietly but relentlessly.

And in the long run, that simple, steady force outperforms every version of market gymnastics you can imagine.